What is IFRS

Keeping financial statements is mandatory for all companies engaged in business activities. It is the study of financial reporting documents that is the very tool on the basis of which a decision is made on the prospects and forms of cooperation between companies. That's why it was created IFRS is a universal financial "language" for companies to communicate internationally.

What is financial reporting

The age of globalization dictates its own conditions for successful business. The activity of many companies implies cooperation with foreign partners, which every year only increases in scale. However, financial systems in different countries are different, which complicates cooperation.

In order for business partners from different countries to be able to "understand each other" without problems, it became necessary to relatively standardize financial information.

As a result, the International Accounting Standards Committee was founded in 1973, which was transformed into the IASB in 2001. The head office of the IASB is located in London.

The IASB is an independent body of the International Financial Reporting Standards Foundation. The IASB develops and publishes international financial reporting standards and approves their interpretations.

What are International Financial Reporting Standards IFRS

IFRS is a set of documents that regulate the conduct of financial statements, which are necessary to represent the activities of the company, according to the same defined principles.

In English-language documents, IFRS looks like an abbreviation IFRS (International Financial Reporting Standards).

IFRS (International Financial Reporting Standard) - is an official translation from English into Russian of a set of documents and their interpretations developed by the IASB.

The entire set of documents in pdf format with a breakdown by sector and an official translation can be found on the council's official website. The official translation into Russian is designated as Blue Book - 2015. In addition, the IFRS documents in Russian are available on the official website of the Ministry of Finance of the Russian Federation.

An example of the first page of an official IFRS translation for business combinations.

At the moment, more than 100 countries fully or partially use IFRS. It is worth noting that the United States and a number of other countries use GAAP (Generally Accepted Accounting Principles).

What is the basic principle of IFRS

The basic meaning of IFRS is that it is not influenced by any differences between countries. Irrespective of national traditions, cultural characteristics, financial system models or legislation, the economic content prevails over the form. This is the main principle of IFRS. In the event of any disputes, it allows companies to follow its spirit rather than seeking to circumvent the strict rules.

In addition to the fundamental principle, IFRS takes into account additional principles governing the preparation of financial statements:

- accrual principle;

- the principle of continuity of activity;

- the principle of relevance.

What an IFRS consists of

The IFRS currently includes 44 documents and 25 clarifications, which provide the following guidance:

- what the financial statements should consist of;

- which method should be used to account for the specific objects of attention of accountants;

- where and exactly what information should be reflected.

It is worth noting that the standards are not dogma; they are periodically updated through various amendments and changes.

All the documents that make up the IFRS can be divided into four levels of hierarchy:

- current standards and their annexes;

- IASB clarifications;

- appendices to the standards that are not included in the official composition;

- recommendations for the implementation of country-specific standards.

IFRS in Russia

Preparation of IFRS financial statements in Russia is regulated by Russian Federal Law № 208-FZ "On Consolidated Financial Statements" dated July 27, 2010.

According to this law, the preparation of financial statements in accordance with IFRS is mandatory for:

- banking organizations;

- insurance companies (except companies for compulsory health insurance);

- mortgage companies;

- commercial pension funds;

- investment companies;

- joint-stock companies with shares owned by the state (according to the list of the Government of the Russian Federation);

- companies whose securities are listed in the official quotes.

At the same time, compliance with IFRS is not mandatory for:

- state-owned companies;

- summary reports of municipal institutions;

- consolidated reporting of budgetary organizations.

This is due to the fact that their activities do not go to the interstate level.

In addition, the standards of IFRS are required to know:

- accountants;

- auditors;

- economic consultants;

- teachers of economic disciplines of higher educational institutions.

IFRS financial statements are publicly available on companies' official websites.

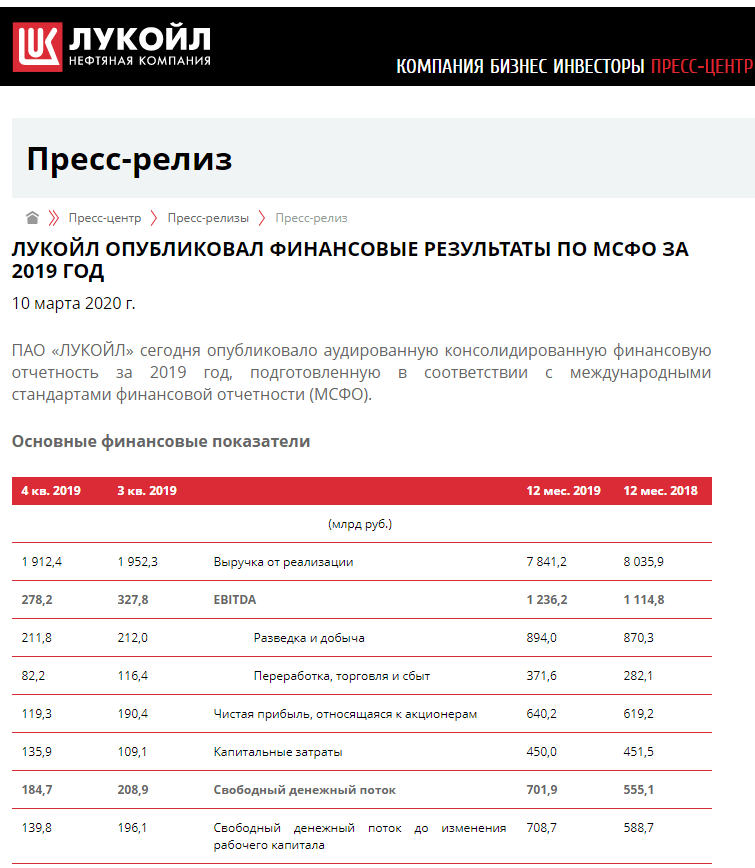

Part of Lukoil's IFRS financial statements at the official website.

Part of Sberbank's IFRS financial statements in pdf format.

Problems with the use of IFRS in Russia

Since the beginning of 2012, in which, according to the Federal Law № 208-FZ, the revision of financial statements according to IFRS was started, a number of difficulties with the implementation and practical application of these standards has been identified:

- language problem

The IFRS documents in Russian posted on the website of the Ministry of Finance are not always accurately translated and do not have the status of an official translation. Official translation of IFRS standards from English into Russian is performed only by the staff of the IASB with subsequent discussion and approval by the relevant experts. Because of this, official translations of IFRS documents appear on the official website with a long delay, and some have not yet been published.

- non-compliance with the fundamental principle of IFRS

As we have already mentioned above, the basic principle of the IFRS is the prevalence of content over form. In the preparation of financial statements by Russian companies, this principle is not always observed. This is due to the rigid rules under which documents accompanying financial activity in the Russian Federation must be drawn up. Consequently, various difficulties arise in bringing the results of accounting to IFRS standards.

- asset valuation problem

The classification of property assets in the Russian Federation differs slightly from the accepted international standards, which makes their valuation difficult. In addition, the market valuation of the asset, which is required in forming the financial indicator, is not always fair.

- legal inconsistencies

Accounting in any country is strictly regulated by laws and other regulations, up to the use of terms defined by the Tax Code. Because of this, when interacting with IFRS norms, certain difficulties arise. At the same time, it is practically impossible to correct such problems at the legislative level.

- information limitation

According to IFRS standards, the amount of publicly available information, for example, about the persons on whom the financial indicators directly depend, is much higher than the information volumes that are traditionally accepted in Russia.