Gazprom shares: forecast for 2020

The price of gas supplied by Gazprom is almost four times higher than quotations on the spot market and is not competitive, leading to a collapse in exports. It is likely that the spring and summer of 2020 will go down in Gazprom's history as the "blackest period" since the start of the 21st century. According to the Central Bank of Russia, Gazprom's export revenues dropped almost threefold in the second quarter, reaching their lowest level in 18 years - $3.5 billion.

How bad is Gazprom's business and what is the future outlook for the company's shares? Alexei Kalachev, an analyst at FINAM, answered Fortrader magazine's question.

Failed Q2 for Gazprom

- Indeed, it appears that the second quarter will be a failure for Gazprom's gas exports. As can be seen from the FCS data, in June, the average price of export sales of natural gas dropped to $94 per thousand cubic meters. Nevertheless, it is still higher than spot prices - which can be explained by the following factors: long-term contracts with their own pricing formula and an emphasis on deferred exports, which, by definition, have a higher price because they guarantee a certain volume of gas at a certain time. At the same time, it is already becoming evident that the gas market has hit rock bottom, and the price is unlikely to go any lower. The pandemic in Europe is subsiding, quarantines are being lifted, and energy demand is still slowly but starting to grow.

- Indeed, it appears that the second quarter will be a failure for Gazprom's gas exports. As can be seen from the FCS data, in June, the average price of export sales of natural gas dropped to $94 per thousand cubic meters. Nevertheless, it is still higher than spot prices - which can be explained by the following factors: long-term contracts with their own pricing formula and an emphasis on deferred exports, which, by definition, have a higher price because they guarantee a certain volume of gas at a certain time. At the same time, it is already becoming evident that the gas market has hit rock bottom, and the price is unlikely to go any lower. The pandemic in Europe is subsiding, quarantines are being lifted, and energy demand is still slowly but starting to grow.

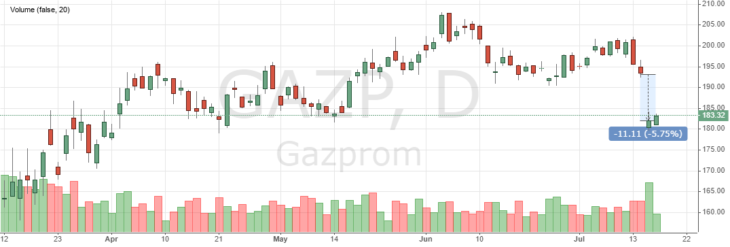

How quickly will Gazprom shares close the dividend gap?

Gazprom shares opened July 15 with a gap down at 6%. This is a dividend gap: yesterday the stock included a record dividend, which the company will pay for last year. 30% of IFRS net income is earmarked for the dividend, the dividend will amount to 15.20 p per share, and the dividend yield was almost 8% by the close of the day.

Gazprom shares. Forecast

In other words, Gazprom trades further without taking these dividends into account. However, although it is a dividend gap, this time we should not expect it to close soon. This year, the company will sharply worsen its financial results, and the market takes that into account. Just yesterday, Gazprom was one of the last to report Q1 2020 results, while the reporting season for the first half of the year has already begun.

Already in the first quarter, Gazprom's sales revenues fell by 24%. At the same time, export revenues from natural gas sales halved. Gas sales to Europe fell by 18% in the first quarter, and the average price fell by 37% to $162 per thousand cubic meters. "Gazprom" showed a net loss for the first time in a long time, which amounted to 116.249 billion rubles against a profit of 535.9 billion rubles received a year earlier.

However, it should be noted that, as in the case of "By Rosneft"The company's currency liabilities are revalued at the last balance sheet date. The revaluation is made as of the last reporting date, and, as we remember, just at the end of March the ruble exchange rate collapsed sharply. Excluding this revaluation, Gazprom would have made a profit of RUB 288 billion. Although this is less than a year earlier, this is the sum from which Gazprom's dividends would have been calculated if it had paid them on a quarterly basis. Taking into account that in 2020 Gazprom is supposed to distribute 40% of net profit to dividends, dividends would have been 4.87 rubles per share. However, this is only an intermediate result, while we should proceed from the final result for the year.

Forecasts are disappointing

We will not see reports for the first half of the year yet, but the operating results of the second quarter so far indicate a worsening of the situation. Only a reverse revaluation of foreign currency liabilities will be beneficial, as the ruble's exchange rate has somewhat regained its value. But gas exports continue to remain low.

April and May saw the peak of the pandemic in Europe, which caused an even greater drop in energy demand. Although gas supplies began to rise as the quarantine was lifted in June, the average price for gas sold for export, as seen in customs data, dropped to $94 per thousand cubic meters.

Everything is already accounted for in stock prices

Speaking about the prospects of Gazprom's shares, we have to proceed from the fact that all this, to a greater or lesser extent, has already been taken into account by the market in their value. As well as the fact that crises do not last forever, and by the end of the year we can expect trends to reverse.

I have distinguished two groups of factors to consider: short-term and long-term.

- Among the short-term ones, there is practically no positive news. And the negative is that the demand for gas due to the pandemic and the general decline in economic activity has dropped sharply, and this was superimposed on a warm winter and the accumulation of record gas reserves in European underground storage facilities.

- And there is only one positive thing, and it is a strong one, which is that all of this is temporary. The pandemic will end, the restrictions will be lifted, and demand will recover.

Long-term forecasts for Gazprom

In the long term, it is foolish to deny that global demand for gas will continue to grow. Gas is not yet the fuel of the past, but it still has promise in the future. Gas will be used more actively in the chemical industry. Gas will replace gasoline in parallel with electric cars, and this process is still in its early days. And most importantly, the importance of gas in the energy sector will continue to grow. In parallel with renewable energy sources, gas will continue to replace coal from the energy balance even more actively. At the same time, while renewable energy technologies increase their efficiency and have an advantage over gas in the production of electrical energy, in the field of thermal energy they are still very, very far away from gas fuel.

LNG and Gazprom

The long-term negative factor for Gazprom, but not for the gas market, is the rapid growth of the liquefied natural gas (LNG) industry.

LNG is radically changing the gas market and making it global and mobile. Gazprom's strategy of building more and more expensive gas pipelines no longer justifies itself.

Thanks to LNG, consumers are increasingly less tied to gas suppliers. LNG can be delivered anywhere, both where there are pipelines and where there are none. As for Gazprom, it remains tied to the markets where it has built a pipeline. But it can no longer count on a monopoly position there. "Gazprom will be losing share in its traditional markets, and in order to keep it, it will have to become more flexible, market-oriented and efficient.

In order to fit into the new era, Gazprom needs to change its strategy, and possibly go through a reform that was previously abandoned.

The gas market is becoming not regional, but global, increasingly similar to the oil market, with a large number of independent players and market pricing. This means that it will be characterized by the same cyclicality in terms of supply and demand and prices.

Medium-term forecasts

In the medium term, I think we can assume that the gas market has hit bottom, and there will be no further decline in demand and prices, but on the contrary, there will be a recovery. A slow recovery at first. But already in the second half of next year, the market will return to pre-crisis growth rates.

Going back to Gazprom shares, I would not expect them to show strong dynamics this year. They are unlikely to rise above 200 rubles per share. However, even in case of negative developments and weak financials, further downside potential will be limited to 150 rubles apiece, where they would be attractive to buy again.